By

By

- This guide walks you through building a money lending app, covering everything from selecting the right lending model and navigating regulatory compliance to finalizing your tech stack and launching an MVP.

- It breaks down essential features like KYC verification, credit scoring, and payment integration while addressing key challenges such as data security and scalability.

- Development typically costs between $25,000 and $250,000+, with timelines ranging from 3 to 12 months.

Key Takeaways:

The global digital lending market is transforming how people access credit. What once required lengthy bank visits and stacks of paperwork now happens in minutes through a smartphone. According to Grand View Research, the global digital lending platform market was valued at USD 10.55 billion in 2024 and is projected to reach USD 44.49 billion by 2030, growing at a CAGR of 27.7% from 2025 to 2030.

As a result, many entrepreneurs, fintech startups, and financial institutions are exploring how to create a money lending app that meets modern borrower expectations while remaining secure and compliant. Whether you’re building an MVP or a full-scale digital lending platform, partnering with an experienced lending app development company can help accelerate development, ensure regulatory compliance, and reduce technical risks.

Whether you’re a startup looking to disrupt traditional lending or an established financial institution aiming to digitize your services, creating a lending app involves navigating complex terrain. From regulatory compliance and secure payment processing to credit risk assessment and user experience design, understanding how to create a money lending mobile app demands the expertise that professional mobile app development services bring to the table.

This guide walks you through the complete process of building a money lending app, from defining your business model and understanding legal requirements to selecting the right tech stack and integrating essential features like KYC verification, credit scoring, and loan management. Whether you plan to build in-house or hire mobile app developers, by the end, you’ll have a clear roadmap for turning your lending app concept into a functional, compliant, and user-friendly product.

Table of Contents

- Money Lending App Types + Examples

- How to Create a Money Lending App [6 Step Process]

- Define Your Lending Model and Validate the Market

- Handle Legal Compliance, Licensing, and Finalize the Tech Stack

- Assemble a Team of Experienced FinTech App Developers

- Build an MVP Version of the Money Lending App

- Perform Thorough App Testing and Publish Your App

- Launch and Promote Your Money Lending App

- Common Challenges in Money Lending App Development and How to Address Them

- Key Systems Your Lending App Must Integrate With

- How Much Does it Cost to Develop a Loan Lending App?

- How Long Does It Take for Loan App Development?

- What Key Features Does A Lending App Have?

- Key Benefits of Money Lending App Development

- Legal Compliance and Encryption for Loan App Development

- Build a Custom Money Lending App with Space-O Technologies

- FAQs About How to Create a Money Lending App

Types of Money Lending Applications with Examples

Before diving into development, you need to decide which lending model aligns with your business goals and target audience. Understanding this foundation is a critical first step in learning how to create a money lending app that is scalable, compliant, and profitable. Each type of application for lending money serves different borrower needs, operates under distinct regulations, and requires specific features.

Here’s a breakdown of the most common money lending app types, along with examples:

1. Peer-to-Peer (P2P) Lending Apps

P2P lending platforms connect individual borrowers directly with investors willing to fund their loans, cutting out traditional financial institutions. The platform acts as an intermediary, handling credit checks, loan agreements, and payment processing while earning revenue through origination fees or interest rate spreads.

-

Examples: LendingClub, Prosper, Upstart, Peerform

Key features required: Investor dashboards, automated loan matching algorithms, risk grading systems, secondary marketplace for loan trading.

2. Payday and Cash Advance Apps

These apps provide small, short-duration loans or earned wage access—allowing users to access a portion of their paycheck before payday. They cater to users who need quick cash for emergencies and often feature simplified approval processes. Many newer apps in this space market themselves as payday loan alternatives with lower or no fees.

-

Examples : Dave, Earnin, Brigit, Chime SpotMe, Albert

Key features required: Payroll integration, income verification, automatic repayment scheduling, spending insights, bank account connectivity

3. Personal Loan Apps

Personal loan apps offer unsecured loans for various purposes—debt consolidation, home improvement, medical expenses, or major purchases. They typically provide larger loan amounts and longer repayment terms than payday apps, with interest rates based on creditworthiness.

-

Examples : SoFi, Upgrade, Upstart, Avant, LightStream, Marcus by Goldman Sachs

Key features required: Comprehensive credit scoring, flexible repayment options, loan calculators, document upload for income verification

4. Business and SME Lending Apps

These platforms focus on providing working capital, equipment financing, or expansion loans to small and medium-sized businesses. They often use alternative data sources—such as cash flow analysis, transaction history, and business performance metrics—to assess creditworthiness beyond traditional credit scores.

-

Examples : Kabbage (now part of American Express), Bluevine, OnDeck, Fundbox, Lendio, Biz2Credit

Key features required: Business account integration, cash flow analysis tools, invoice financing options, merchant dashboard

5. Buy Now, Pay Later (BNPL) Apps

BNPL apps allow consumers to split purchases into interest-free installments at the point of sale. These platforms partner with retailers and e-commerce merchants, generating revenue through merchant fees rather than borrower interest. The model has seen rapid adoption among American consumers, particularly millennials and Gen Z.

-

Examples : Affirm, Klarna, Afterpay, Sezzle, Zip (formerly Quadpay), PayPal Pay in 4

Key features required: Merchant integration APIs, virtual card generation, installment tracking, retail partner portal

6. Student Loan Apps

These platforms offer student loan refinancing, private student loans, or tools for managing existing education debt. Given the scale of student debt in America, this category has significant market demand and continues to attract both startups and established financial institutions.

-

Examples : SoFi, Earnest, CommonBond, Splash Financial, College Ave

Key features required: Refinancing calculators, federal vs. private loan comparison tools, income-driven repayment options, and co-signer release features

7. Mortgage and Home Loan Apps

Digital mortgage platforms streamline the traditionally complex home-buying process by offering online applications, document uploads, rate comparisons, and loan tracking. These apps require robust compliance frameworks given the heavily regulated nature of mortgage lending in the US.

-

Examples : Rocket Mortgage, Better.com, LoanDepot, SoFi Home Loans, Guaranteed Rate

Key features required: Property valuation tools, document management systems, e-signature integration, rate lock functionality, compliance automation

8. Microfinance and Micro-lending Apps

Microfinance apps deliver small, collateral-free loans to underbanked users like gig workers and rural communities using alternative credit scoring instead of traditional methods. With platforms like Tala and Branch proving scalability across emerging markets, launching a micro loan app in this segment offers fintech startups high transaction volumes and strong repeat borrowing potential.

-

Examples : Tala, Branch, Kiva, Jumo, FairMoney

Key features required: Mobile-first onboarding with minimal documentation, alternative credit scoring using non-traditional data, automated micro-disbursement to mobile wallets, SMS and push-based repayment reminders, financial literacy modules for first-time borrowers

9. Crypto and DeFi Lending Apps

Cryptocurrency lending apps let users borrow against crypto holdings or lend digital assets to earn interest through centralized platforms like Nexo or decentralized protocols like Aave and Compound. Smart contracts automate loan agreements, collateral management, and liquidations, reducing manual processing significantly. With regulations from bodies like the SEC still evolving, building regulatory flexibility into the platform is a critical design consideration.

-

Examples : Aave, Compound, Nexo, YouHodler, CoinLoan

Key features required: Crypto wallet integration, smart contract-based loan execution, real-time collateral monitoring with automated liquidation, multi-chain support (Ethereum, Solana, Polygon), fiat on-ramp and off-ramp integration, transparent APY display for lenders

10. Loan Management and Servicing Platforms

Loan management and servicing platforms serve banks, NBFCs, and lending companies by handling the post-origination lifecycle, including billing, collections, payment tracking, delinquency management, and regulatory reporting. These platforms also offer borrower self-service portals that reduce support volumes while improving satisfaction. For fintech companies focused on B2B, this segment offers strong revenue through licensing fees, per-loan charges, and white-label solutions.

-

Examples : Loan Pro, Mortgage Cadence, Bryt Software, TurnKey Lender

Key features required: Loan portfolio dashboard with real-time status tracking, automated billing and payment processing, delinquency and collections workflow management, borrower self-service portal, regulatory reporting modules for compliance audits, integration with core banking systems and accounting software

Want to Validate Your Money Lending App Idea?

Contact us. Our experienced lending app development team validates your idea and provide you the roadmap to proceed further.

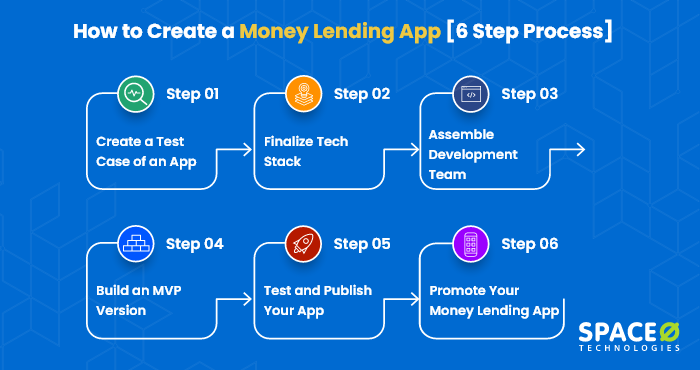

How to Create a Money Lending App [6 Step Process]

Creating a money lending app requires a careful balance of legal compliance, robust security, and a seamless user experience. The process involves defining a specific lending model, conducting market research, securing licenses, choosing a tech stack, assembling a development team, and building a Minimum Viable Product (MVP).

Building a successful lending platform involves navigating several core phases:

-

Define Your Lending Model and Validate the Market

Having a money lending app idea is the first step in the loan app development process. Knowing how to create a loan app starts with selecting the right lending model for your target market. Start by deciding how your app will function:

- Peer-to-Peer (P2P): Connects individual borrowers with individual investors or lenders.

- Direct Lender: Your business issues loans directly from its own capital pool.

- Microfinance/Payday: Short-term, small-amount loans meant for quick approval.

Once you have selected a lending model and determined how to start a loan app business, validate the idea through detailed market research. Study your competitors by reviewing their app store ratings, user feedback, and feature sets. Analyze business listing platforms like G2, Clutch, and Capterra to understand what existing lending apps offer and how they monetize.

Steps to follow Explanation Competitor Reviews - Check your competitor’s reviews and ratings

- Target FinTech industry and money lending companies

- Check comments of existing userbase

App Features - Go to Play Store, App Store, install the app to check the features and design of the app

- Check competitor’s website to find their services and functionalities

Analyze Business Listing Websites Set the filter according to business categories, articles, and relevance. By doing this you will be able to know what your competitors are providing in their application and their monetization strategy. - G2

- Clutch

- Capterra

This research helps you identify gaps in the market, define your target audience, and build a product with a clear competitive advantage. Another key element to remember is to build your loan app from a futuristic point of view. During your product development, you need to think about the functionalities, technologies, and scalability. As the demands will increase in the future, you will be responsible for scaling your money lending platform with the latest features and functionalities.

-

Handle Legal Compliance, Licensing, and Finalize the Tech Stack

Financial technology (Fintech) is highly regulated, and loan lending mobile app development in USA requires navigating both federal and state-level compliance frameworks. Depending on your jurisdiction (e.g., the EU or US), you will need:

- Lending Licenses: Obtain the necessary local licenses to originate or broker loans.

- KYC/AML (Know Your Customer / Anti-Money Laundering): Integrate identity verification services to prevent fraud and confirm user identities.

- Data Protection: Ensure your app aligns with regional privacy laws (such as the GDPR in Europe).

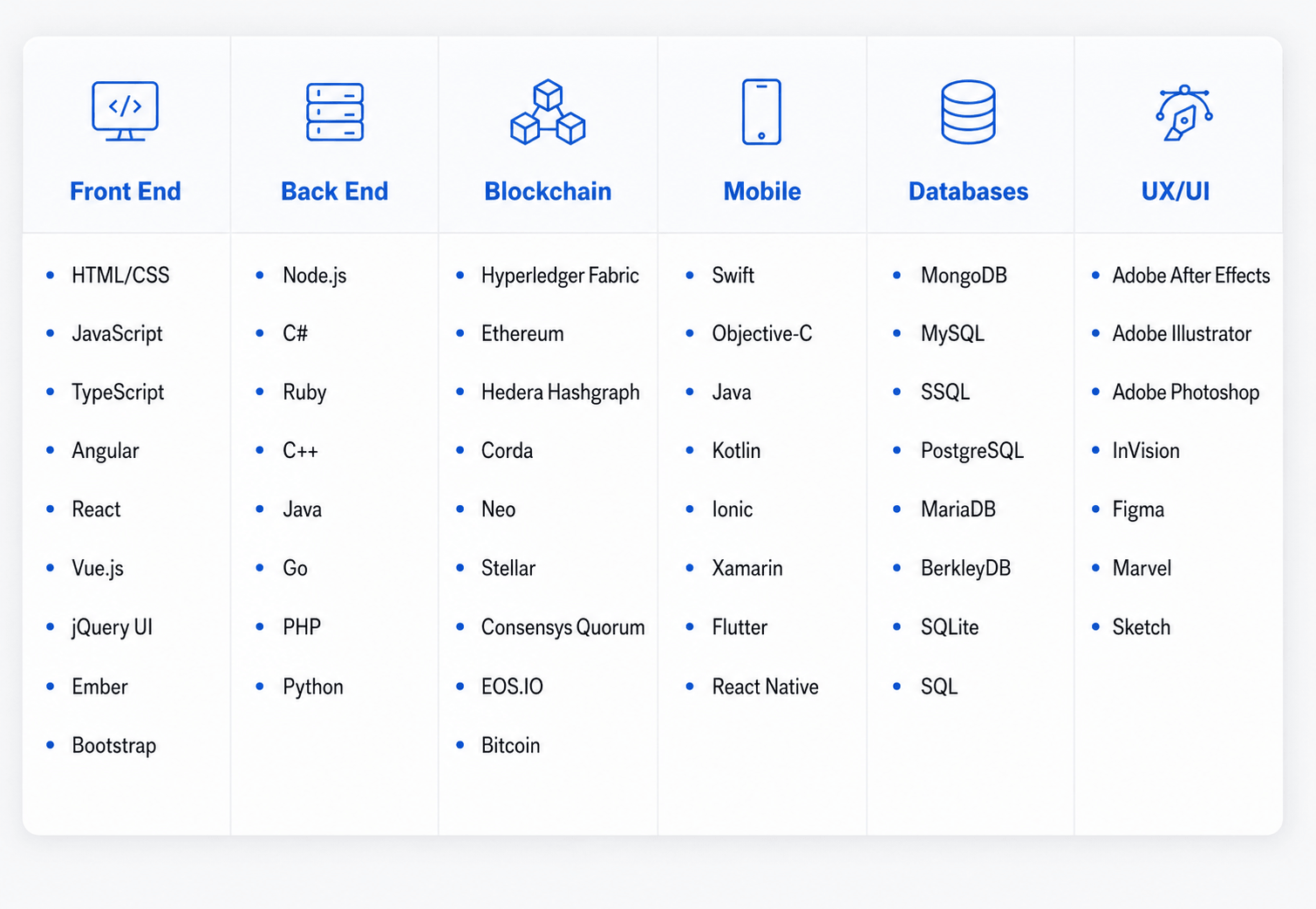

Once compliance requirements are mapped, finalize the technology stack. Choosing the right technology stack is important to build scalable money lending apps. To build a highly scalable and secure app, developers typically rely on:

- Frontend: Cross-platform frameworks used for React Native / Flutter development to build for both iOS and Android simultaneously.

- Backend & Cloud: AWS / Azure cloud infrastructure for scalable, cloud-native deployments using services like Lambda, EC2, API Gateway, and managed databases.

- Payment Gateways: APIs like Stripe or Plaid to manage bank connections and money transfers safely.

The below image shows the list of technologies that are used for web and mobile application development. FinTech applications use these technologies to build their mobile applications. This technology stack is not limited to only building money lending apps but covers the entire FinTech industry.

Alongside the tech stack, plan for core features your app must include: separate user portals for borrowers and lenders, a credit scoring module integrated with external credit bureaus, e-signature and document upload functionality, and a repayment dashboard for managing loan status, repayment schedules, and automated bank debits.

Even using the latest technology stack, we have built FinTech solutions for our client. Have a look.

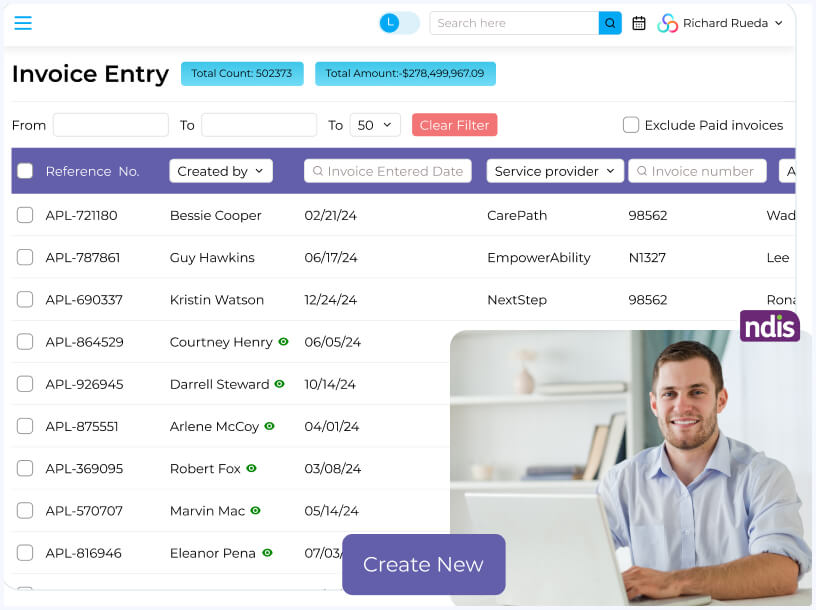

RaeCRM: NDIS Fund Management Software

A secure NDIS fund management solution that helps participants, coordinators, and service providers efficiently manage budgets, process invoices, and track claims through a centralized web portal. Built using Laravel, MySQL, and Amazon S3.

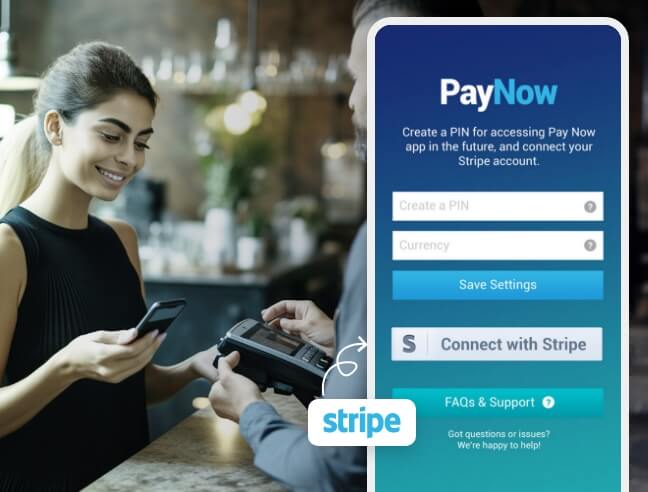

PayNow: Payment & Point of Sale App for Stripe

A mobile point-of-sale app that lets small business vendors accept credit card payments via Stripe directly from their phones. The app generated 35x ROI, gained 50,000+ users, and ranked 3rd in top innovative apps in Australia.

CharityCalc: Gift Annuity Calculator App

A fintech app that helps nonprofit organizations and financial advisors calculate annuity rates, estimate tax deductions, and generate gift annuity illustrations for donors through a simple mobile interface.

-

Assemble a Team of Experienced FinTech App Developers

A lending app requires a well-rounded team with experience in fintech development. To develop your lending app successfully, hire a dedicated team, on-site team, or follow a fixed price model or hourly price model depending upon your project requirements.

However, it is best to assign the project to an experienced loan lending app development company with past experience in building FinTech related mobile app solutions. Therefore, the below entities are required to complete your money lending mobile application development project successfully.

- Team lead

- UI/UX

- Front end developers

- Back end developers

- iOS and Android developers

- QA specialist

- Project manager

Being a reputed mobile app development company, we have more than 200 experienced developers who have built more than 4400 mobile apps. Partnering with a team that has prior fintech experience is highly recommended, as they will already understand the regulatory, security, and integration requirements specific to lending platforms.

-

Build an MVP Version of the Money Lending App

As Eric Ries, a well-known American entrepreneur quotes, “A minimal viable product is a version of a new product that allows a team to gather the most amount of validated customer learning with the least amount of effort.”

Rather than building every planned feature at once, begin with MVP development that includes only the core lending functionality. An MVP allows you to test your app with real users, collect early feedback, and validate demand before committing to full-scale development. If you are exploring how to create a loan app efficiently, contact an app development company to build MVP as it helps you develop MVP version as per your custom requirements.

- Initially, check the viability of your application with good user interface without investing much of your effort and money. If your target audience is not interested in your app, then you will regret over-investing. However, by building MVP initially, you will have the advantage of building the entire product right away.

- You’ll know whether or not people need your product, and if so, for what and how they’ll utilize it. You will get quick feedback to optimize your app accordingly.

- By developing an MVP version, you will understand what is working and the modifications you require for your mobile app. By receiving negative feedback, the core part of your mobile app may change. However, this is the better option, and you will understand what is in demand right now.

- If the MVP launch goes well, you’ll start making money and gaining clients long before the full version is ready. You’ll see a quick return on investment and locate users who are more likely to become regular customers as a result of this.

In addition, people may not need some of the features that you planned to spend a lot of time and effort on. Ignoring those features will help you reduce cost and time and allow you to focus on what your target audience needs the most. After the MVP development ends, the step will be to test and publish the application.

-

Perform Thorough App Testing and Publish Your App

Your job doesn’t end after building the MVP version of the app. Thorough testing is a critical phase of loan lending app development, and it is essential to test your mobile app strategically to ensure its superior quality output. If you are developing an app from an app development company, the company tests the app for you. Here are some of the test methods to follow.

Elements to Test Explanation Automation Automation integration is necessary to increase app efficiency. It also helps to increase product quality and decrease manual effort. App Security Personal data protection monitored compliance and high API security should be tested. Data Integration - Validating and preserving stored data

- Transferring and exchanging data

- Test account accessibility

- Two-factor authentication

Functionality Functionalities should be tested using a regression testing method.

Expected app functionalities such as account opening, bill payment, and deposits process should work seamlessly.Performance Testing While applying for business loans, some instant loan apps crash; this is a sign of poor app testing. Your app should not crash even while having an increasing amount of user base. Once testing is complete, submit your app to the Apple App Store and Google Play Store, ensuring your listing meets all platform-specific guidelines for financial applications.

-

Launch and Promote Your Money Lending App

After successfully testing your mobile app, launch your app. A strong launch strategy is essential to drive initial user adoption and maximize the returns on your loan lending app development investment. Here are 3 ways to market your P2P money lending app.

-

Promote an App via Landing Page

Design a landing page with intuitive design and engaging content to drive maximum conversion for your lending app. Even a website is an essential tool for generating quality leads for your money lending app. Design a simple yet intuitive landing page to get maximum exposure from users.

To get inspiration, check the websites of leading money lending businesses in the USA, such as Earnin and Dave.

-

Social Media Marketing

There are 4.59 billion social network users across the world. Platforms like Facebook, LinkedIn, and YouTube consist of a higher user base, where you can promote your money lending app to targeted demographics including small business owners, freelancers, and underserved borrowers.

-

Content Marketing

In a poll of worldwide marketers, 91% of respondents stated that content marketing was already being used as part of their promotional activities. Blog post creation, educational guides, video marketing, and eBook writing are some ways to promote your brand as well as your app to the end-user while building organic visibility in the lending space.

-

Your end goal should be to monetize your money lending app successfully. If you are figuring out how to start an online money lending business, a solid monetization strategy combined with a strong launch plan is essential. By having enough finance, you will be able to scale your lending business.

Common Challenges in Money Lending App Development and How to Address Them

Building a money lending app is not just a technical exercise. It involves navigating regulatory complexity, managing sensitive financial data, and solving real engineering problems around scalability and system integration. Here are the most common challenges development teams face and practical ways to address them.

1. Navigating Constantly Changing Regulations

Lending laws vary by country, state, and even city. In the US alone, you need to account for TILA, ECOA, FCRA, and state-specific licensing rules. Operating in the EU adds GDPR obligations. In India, NBFC regulations governed by the Reserve Bank of India (RBI) impose strict requirements around capital adequacy, fair lending practices, digital lending guidelines, and borrower data privacy that any lending app targeting the Indian market must comply with. And these regulations keep evolving, so a feature that was compliant at launch may fall out of compliance months later.

How to address it during development:

- Build your app architecture with modular compliance layers that can be updated independently of the core lending logic.

- Partner with a fintech-specialized legal advisor from day one and schedule quarterly compliance audits into your roadmap.

- For multi-geography apps, implement region-specific rule engines that automatically apply the correct regulatory framework based on the user’s location.

- Subscribe to regulatory update feeds from bodies like the CFPB and SEC so your team is notified the moment new rules are proposed or enacted.

2. Ensuring Data Security and Fraud Prevention

A lending app handles highly sensitive data: Social Security numbers, bank account details, income documents, and credit reports. A single breach can destroy user trust and trigger regulatory penalties. Beyond external threats, fraud risks like synthetic identity fraud, loan stacking, and document forgery are growing concerns across the digital lending industry.

How to address it during development:

- Implement end-to-end encryption for all data in transit (TLS 1.3) and at rest (AES-256) across every component of your application.

- Use multi-factor authentication combining password, OTP, and biometric verification for both borrower and admin logins.

- Integrate AI-powered fraud detection that flags suspicious patterns in real time, such as multiple applications from the same device or mismatched identity documents.

- Conduct penetration testing at least quarterly and maintain PCI DSS compliance for all payment-related data handling.

- Implement device fingerprinting and velocity checks to detect loan stacking and synthetic identity fraud before disbursement.

3. Building Accurate Credit Scoring for Underserved Borrowers

Traditional credit scoring works well for borrowers with established histories but excludes millions of potential users like gig workers, young professionals, immigrants, and people in developing economies. Alternative scoring models help fill this gap, but if poorly designed, they can introduce bias or run into fair lending violations.

How to address it during development:

- Combine traditional credit bureau data with alternative signals such as bank transaction history, rent payments, utility bill consistency, and employment verification through payroll APIs.

- Use machine learning models that are regularly retrained on updated loan performance data to improve prediction accuracy over time.

- Build explainability into your scoring system so the model generates clear, human-readable reasons for every approval or denial.

- Test scoring models for demographic bias before deployment and conduct periodic fairness audits for equal credit opportunity compliance.

- Partner with alternative data providers like Plaid, Nova Credit, or Petal to access non-traditional data streams for thin-file borrowers.

4. Managing Complex Third-party Integrations

A lending app needs to communicate with payment gateways, credit bureaus, KYC/AML providers, banking APIs, and accounting software. Each integration has its own API standards, authentication requirements, and failure modes. The real challenge is not just making them work initially but keeping them stable as providers update their APIs or experience downtime.

How to address it during development:

- Use an API gateway or middleware layer as a buffer between your core logic and external services, making it easier to swap providers and handle versioning.

- Build retry mechanisms and fallback options for critical integrations like payment processing so third-party outages do not block disbursements or repayments.

- Maintain comprehensive internal API documentation for every integration, including authentication flows, response formats, and error codes.

- Set up automated monitoring that alerts your team immediately when any integration endpoint returns errors or experiences latency spikes.

- Use webhook-based event-driven architecture instead of polling to reduce API call volume and improve real-time data synchronization.

5. Scaling Infrastructure Under Unpredictable Load

Marketing campaigns, partnership launches, or economic events like interest rate changes can drive sudden surges in loan applications. If your infrastructure is not designed for elastic scaling, the app may crash during exactly the moments when users need it most.

How to address it during development:

- Build on cloud-native infrastructure (AWS, Azure, or GCP) using containerized microservices orchestrated through Kubernetes so individual components like loan processing and KYC verification scale independently.

- Implement auto-scaling policies that add server capacity during traffic spikes and reduce it during low-activity periods to control costs.

- Make load testing a standard part of QA, simulating 3x to 5x your expected peak traffic to identify bottlenecks before they affect real users.

- Use a CDN for static assets and implement database read replicas to distribute query load during high-traffic periods.

- Review infrastructure capacity monthly, tracking concurrent sessions, transaction volume, and database performance to forecast scaling needs proactively. These infrastructure decisions are foundational for anyone learning how to build a loan app that performs reliably under real-world conditions.

Developing a successful money lending app requires more than building core lending features. From regulatory compliance and fraud prevention to credit scoring, third-party integrations, and infrastructure scalability, each challenge demands careful planning and the right technology strategy. By addressing these complexities early in the development process, businesses exploring how to create a money lending app can build secure, compliant, and scalable lending platforms that deliver a seamless user experience while supporting long-term growth in an increasingly competitive fintech landscape.

Key Systems Your Lending App Must Integrate With

A money lending app does not function as a standalone product. It needs to connect with multiple external systems and services to handle everything from identity verification to payment processing. Below are the critical integration points for any lending platform.

1. Payment Gateways and Banking APIs

Your app needs to process loan disbursements and collect repayments securely. Integration with payment gateways like Stripe, PayPal, Razorpay, or Plaid enables bank account connectivity, ACH transfers, card payments, and digital wallet transactions. For apps operating in multiple countries, you may need region-specific payment providers to support local payment methods and currencies.

Open banking APIs (such as Plaid in the US or Yodlee globally) allow your app to securely access borrower bank account data for income verification, cash flow analysis, and automatic repayment setup without requiring users to share their banking credentials directly.

2. Credit Bureaus and Scoring Services

To assess borrower creditworthiness, your app needs to pull credit reports and scores from major credit bureaus. In the US, this means integrating with Equifax, Experian, and TransUnion through their respective APIs. For apps targeting the Indian market, CIBIL integration is essential, as CIBIL (now TransUnion CIBIL) is the primary credit bureau used by banks, NBFCs, and digital lenders in India to assess borrower creditworthiness and generate credit scores.

For alternative credit scoring, services like Nova Credit (for immigrant borrowers), Plaid (for transaction-based scoring), or custom ML models trained on your platform’s historical data can supplement traditional bureau data.

3. KYC/AML Verification Providers

Regulatory compliance requires verifying borrower identity and screening against anti-money laundering watchlists. Third-party KYC providers like Jumio, Onfido, Socure, or Trulioo handle document verification (ID scans, selfie matching), identity validation, and sanctions list screening through API integrations. These services significantly speed up the onboarding process while maintaining compliance with AML/CFT and OFAC requirements.

4. Loan Origination and Management Systems

If your app is being developed for an existing financial institution, it will likely need to connect with the institution’s loan origination system (LOS) or loan management system (LMS). These backend platforms handle underwriting workflows, loan document generation, compliance checks, and portfolio management. Popular LOS/LMS platforms include Encompass, LoanPro, and Finastra, each offering API-based integration options.

5. Accounting and ERP Systems

For business lending apps and platforms serving institutional lenders, integration with accounting software (QuickBooks, Xero, FreshBooks) and enterprise resource planning systems (SAP, Oracle NetSuite) enables automated financial reconciliation, tax reporting, and cash flow tracking. This is especially important for SME lending apps where borrower financial data often lives inside accounting tools rather than bank statements.

6. Communication and Notification Services

Lending apps need reliable communication channels for transaction alerts, payment reminders, application status updates, and marketing messages. Integration with services like Twilio (for SMS and voice), SendGrid or Amazon SES (for email), and Firebase Cloud Messaging (for push notifications) ensures timely and consistent communication across all channels.

7. E-signature and Document Management

Digital loan agreements require legally binding electronic signatures. Integration with e-signature platforms like DocuSign, Adobe Sign, or HelloSign eliminates the need for physical paperwork and accelerates the loan closing process. For document storage and management, cloud services like AWS S3 or Google Cloud Storage provide secure, scalable repositories for loan agreements, identity documents, and compliance records.

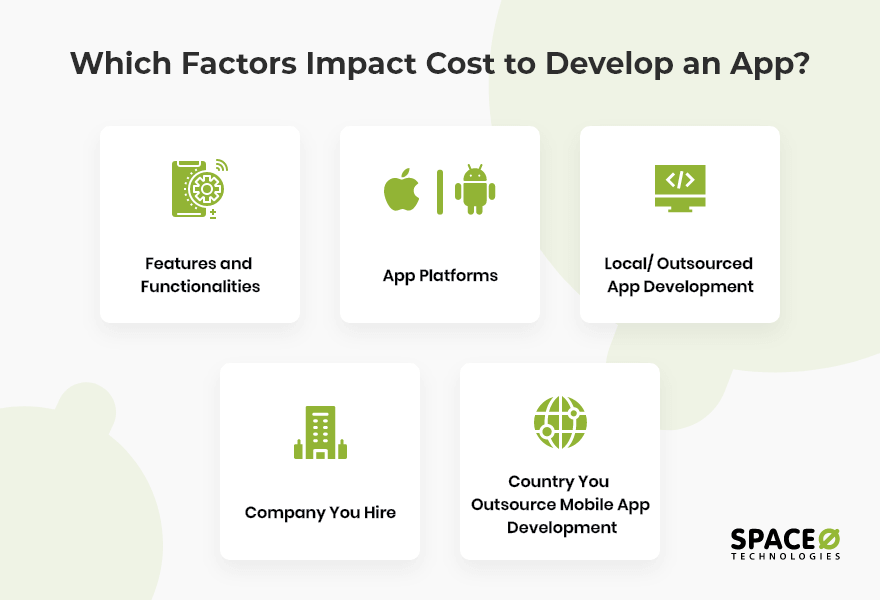

How Much Does it Cost to Develop a Loan Lending App?

The cost to build a money lending app may range between $25,000 to more than $250,000 depending upon factors such as app functionalities and features. To know more about app development cost to build a money lending app, check the below image that mentions the factors directly impacting the loan lending app development cost.

Understanding these key factors will help you make informed decisions about your fintech app development cost and better estimate the overall loan lending app development cost for your specific project scope. Partner with experienced developers who can deliver a secure, compliant, and user-friendly money lending solution within your budget.

How Long Does It Take for Loan App Development?

After discussing the app development cost, next we have curated an estimated timeline to build a money lending app.

| Money Lending App Development Process | Estimated Man Hours | |

|---|---|---|

| iOS | Android | |

| Wireframing | 40 hours | 40 hours |

| Design | 45 hours | 45 hours |

| SRS | 35 hours | 35 hours |

| Test Case | 30 hours | 30 hours |

| App Development | 220 hours | 220 hours |

| Backend Development | 160 hours | 160 hours |

| App Testing | 40 Hours | 40 Hours |

| Total Hours | 570 Hours | 570 Hours |

This isn’t the end of the schedule for loan lending app development. We’ve also provided a rough timeline based on the many sorts of educational apps.

| Top Features of Money Lending App | Estimated Man Hours | |

|---|---|---|

| iOS | Android | |

| Loan Management | 52+ Hours | 52+ Hours |

| Payment and Billing | 40+ Hours | 40+ Hours |

| EMIs and Transactions | 52+ Hours | 52+ Hours |

| Withdrawals and Transfer | 170+ Hours | 170+ Hours |

Want to Develop Customised Money Lending App Solution?

Talk to us. Share your P2P money lending app idea with our app consultant and our experienced team will help you to build a customized solution.

What Key Features Does A Money Lending App Have?

Building a successful money lending app requires thoughtful integration of features that serve both lenders and borrowers while maintaining security and compliance. Whether you’re developing a peer-to-peer lending platform, a microfinance solution, or a digital loan marketplace, understanding how to create a money lending app that earns user trust starts with selecting the right core features for your target market and building trust in your platform.

1. User Registration and KYC Verification

The foundation of any lending app begins with secure user onboarding. Modern lending platforms implement multi-step registration processes that collect essential personal information, verify identities, and ensure regulatory compliance. KYC & compliance verification typically includes document uploads such as government-issued IDs, proof of address, and sometimes biometric authentication. This process not only meets legal requirements but also helps prevent fraud and builds credibility in your platform.

2. Credit Scoring and Risk Assessment

One of the most critical features distinguishing lending apps from traditional banking is automated credit scoring & underwriting. Advanced algorithms analyze multiple data points including credit history, income verification, employment status, banking transactions, and even alternative data like utility payments or social behavior. This AI-driven approach enables faster loan approvals while maintaining appropriate risk management, often providing opportunities to underserved populations who might lack traditional credit histories.

3. Loan Application and Management

A streamlined loan application process is essential for user satisfaction. The best lending apps allow borrowers to apply for loans in minutes, not days. This includes features like loan calculators that help users understand their potential payments, customizable loan amounts and terms, instant eligibility checks, and real-time application tracking. Effective borrower & lender management is equally important. Once approved, borrowers should be able to view their loan details, repayment schedules, outstanding balances, and transaction history all within the app, while lenders get dedicated dashboards to track disbursements, returns, and portfolio health.

4. Secure Payment Integration

Multiple payment options are crucial for both disbursement and repayment. Integration with various payment gateways, bank transfers, digital wallets, and even cryptocurrency options (where applicable) provides flexibility to users. Built-in loan repayment & EMI tracking with automated deductions, payment reminders, due date calendars, and early repayment options enhance the user experience while improving collection rates.

5. Document Management System

Digital lending eliminates paperwork through cloud-based document storage. Users can upload, store, and manage all loan-related documents securely within the app. This includes loan agreements, repayment schedules, tax documents, and correspondence history. Both borrowers and lenders benefit from having instant access to their documents anytime, anywhere.

6. Real-Time Notifications and Alerts

Keeping users informed at every step builds trust and improves engagement. Push notifications, SMS alerts, and email updates should cover loan application status, approval or rejection notifications, payment due dates and reminders, successful payment confirmations, changes to interest rates or terms, and promotional offers for existing customers.

7. Customer Support and Chatbot

Accessible customer service is non-negotiable in financial services. Modern lending apps incorporate AI-powered chatbots for instant responses to common queries, in-app messaging with support teams, comprehensive FAQ sections, and options for phone or video support when needed. The ability to resolve issues quickly directly impacts user satisfaction and retention.

8. Analytics and Reporting Dashboard

For both administrators and users, data visibility is important. Borrowers appreciate seeing their credit improvement over time, payment history visualizations, and interest saved through early payments. Meanwhile, lenders and platform administrators need robust dashboards showing portfolio performance, default rates, user acquisition metrics, and revenue analytics.

9. Referral Programs and Rewards

Growth often comes through word-of-mouth in the fintech space. Built-in referral systems that reward users for bringing new borrowers or lenders to the platform can significantly accelerate user acquisition. This might include cashback offers, reduced interest rates, or bonus credits.

10. Security Features

Financial apps are prime targets for cybercriminals, making robust data security & encryption essential. This includes end-to-end encryption (TLS 1.3 and AES-256) for all data transmission and storage, two-factor authentication, biometric login options, automatic logout after inactivity, fraud detection algorithms, and regular security audits. Users need confidence that their financial and personal information is protected.

Key Benefits of Money Lending App Development

Building a money lending app creates competitive advantages that traditional lending can’t match. Digital lending apps are reshaping the financial services industry by offering faster, more accessible, and cost-effective alternatives to conventional loan processes.

1. Faster Loan Processing and Disbursement

Traditional bank loans take 5-15 business days. Digital lending apps compress this to minutes through automated document verification, real-time credit checks, and instant KYC processing. Borrowers get funds faster while lenders process higher volumes without increasing headcount—the primary reason users are shifting to mobile-first platforms.

2. Smarter Risk Assessment with AI-Powered Credit Scoring

Modern lending apps use machine learning to analyze alternative data: bank transactions, utility payments, payroll data, and behavioral signals. This improves approval accuracy for creditworthy borrowers with thin credit files and opens underserved markets. AI-driven underwriting handles approximately 44% of digital lending decisions and has improved approval rates by 25% without increasing portfolio risk.

3. Lower Operational Costs at Scale

Digital platforms automate loan origination, document collection, disbursement, and repayment tracking. This significantly reduces cost-per-loan, allowing you to service 10x more borrowers with the same team while offering competitive rates.

4. Multiple Revenue Streams Beyond Interest

Lending apps support diverse monetization: origination fees (1-6% of loan amount), late payment fees, premium subscriptions, cross-selling insurance and credit monitoring, partner commissions, and white-label licensing. This revenue diversification builds resilience and scalability.

5. Built-In Regulatory Compliance

Well-designed apps integrate compliance into standard workflows: automated KYC/AML verification, real-time regulatory reporting, PCI DSS-compliant encrypted storage, transaction audit trails, and adherence to TILA, ECOA, FCRA, and CCPA. This reduces compliance overhead and violation risks.

6. Higher Customer Retention and Lifetime Value

Mobile apps create ongoing engagement through personalized loan offers, automated payment reminders, in-app credit tracking, loyalty rewards, and seamless refinancing. This lowers customer acquisition costs (CAC) and increases lifetime value (LTV)—critical metrics for sustainable growth.

7. Broader Market Reach Through Financial Inclusion

Traditional banks exclude millions lacking formal credit history: gig workers, freelancers, immigrants, students. Lending apps with alternative credit scoring, mobile-first onboarding, and collateral-free microloans serve these segments profitably. According to Grand View Research, the US digital lending market generated a revenue of USD 2,420.9 million in 2024 and projected to hit USD 9,583.3 million by 2030, digital lending apps are empowering digital-first lenders to embrace financial inclusion, and opportunities in this space continue expanding.

Money lending app development isn’t just digitization—it’s a strategic transformation enabling faster processing, smarter risk assessment, lower costs, diversified revenue, automated compliance, stronger retention, and broader market access in a rapidly growing industry. These advantages demonstrate why knowing how to create a money lending app with the right foundation is critical for long-term success in digital lending.

Legal Compliance and Encryption for Loan App Development

If you have decided to go fully-fledged with your loan apps business idea and build money transfer app solutions, you should take some precautions to avoid fines and penalties. Even it is essential for you to protect your app from malefactors. So by applying the following points, you can easily protect your app from hacking, user data breach and secure your mobile app.

| Compliance and Encryption Points | Explanation |

|---|---|

| Seamless Working of App | Developers need to consider P2P lending apps to be fault-tolerant. It will work uninterruptedly even if a heavy load due to a large number of simultaneous operations may occur. Therefore, it is required for a developer to use tools that will handle fault tolerance. |

| Prioritize Security | Integrate biometric authentication and two-factor authentication. Apart from that, make use of APIs to safeguard user data. To keep your app safe from fraudulent actions and cybercrime the connection from the P2P platform to servers should be encrypted. |

| GDPR Compliance | If you are launching loan apps in the EU (European Union) market, making a GDPR compliant app is crucial. This regulation became officially effective on May 25, 2018. If you don’t want to be fined, you should follow these steps to make the lending process seamless. |

| CCPA Compliance | The aim of the California Consumer Privacy Act (CCPA) is to secure users’ private data for California residents. It is necessary for the users to have total authority over their personal data. CCPA became official on Jan 1, 2020. Therefore, if California is your target market, it is essential to make your mobile loan app CCPA compliant. |

Build a Custom Money Lending App with Space-O Technologies

Building a money lending app involves much more than developing core features. Success depends on creating a secure, scalable, and compliant platform that delivers a seamless borrowing experience while meeting regulatory requirements. From KYC verification and credit scoring to payment integrations and loan management, every component plays a critical role in the success of your lending business.

As covered in this guide, creating a digital lending platform requires careful planning, the right technology stack, robust security measures, and a clear understanding of industry regulations. Working with an experienced financial software development company can help you navigate these complexities and bring your product to market faster.

With 14+ years of experience and 300+ successful software projects delivered globally, Space-O Technologies helps startups, fintech companies, and enterprises understand how to create a money lending mobile app with customized lending solutions tailored to their unique business needs. Our loan lending app development services cover end-to-end delivery, and our team specializes in developing secure and scalable money lending apps with features such as automated loan processing, credit assessment, KYC verification, payment gateway integration, and real-time analytics.

Whether you are planning to launch a payday loan app, peer-to-peer lending platform, microfinance application, or a complete digital lending ecosystem, our experts can guide you through every stage of the development process.

Book a consultation with our fintech specialists to validate your idea, discuss your requirements, and build a money lending app that drives business growth and delivers an exceptional user experience.

FAQs on How to Create a Money Lending App

How much does it cost to build a money lending app?

The cost of developing a money lending app typically ranges from $50,000 to $250,000, depending on feature complexity, lending model, compliance requirements, and third-party integrations. Major cost factors include security infrastructure, credit assessment systems, payment integrations, and platform selection, whether iOS, Android, or cross-platform.

How do loan mobile apps work?

A typical application for lending money follows this process:

- Download the app and register a new account.

- Complete KYC verification (government ID, proof of address, selfie).

- Enter desired loan amount and repayment term.

- The app runs automated credit assessment to determine eligibility and interest rate.

- Review the offer, accept terms, and provide e-signature.

- Link your bank account for disbursement and automated repayment.

Once approved, funds are disbursed to your bank account with confirmation via email, SMS, and in-app notification. This streamlined process is what separates the best instant loan app platforms from traditional lenders.

How long does it take to develop a money lending app?

A basic lending app MVP typically takes 3 to 4 months to develop. A fully featured digital lending platform with advanced underwriting, compliance workflows, and third-party integrations may require 6 to 12 months. Development timelines depend on project scope, regulatory requirements, integrations, and team size.

What features are essential for a money lending app?

Core features include user registration, KYC verification, credit scoring, loan application management, payment gateway integration, EMI tracking, loan management dashboards, borrower and lender portals, and secure data encryption. Advanced platforms may also include AI-driven risk assessment, fraud detection, and automated underwriting systems.

How do lending apps make money?

Lending apps generate revenue through interest charges, loan origination fees, late payment penalties, subscription plans, and merchant partnerships. Some platforms also earn through cross-selling financial products, referral commissions, and white-label licensing of their lending technology.

Do I need a license to lend money?

Yes, lending activities are regulated in most jurisdictions. Licensing requirements vary by country and region. In the United States, lenders must comply with state licensing requirements and federal regulations. In India, digital lending businesses must follow RBI guidelines and applicable NBFC regulations. Legal consultation is recommended before launching a lending platform.

Is a money lending business profitable?

Yes, digital lending can be highly profitable when supported by effective risk management and compliance processes. Revenue is generated through interest income, service fees, subscriptions, and partner commissions. Automation also helps reduce operational costs, improving overall profit margins as the business scales.

Do I need an LLC to create a money lending app?

While an LLC is not always legally required to develop an app, it is strongly recommended for lending businesses. An LLC helps separate personal and business liabilities, provides legal protection, and supports licensing and regulatory compliance requirements. Consult a qualified attorney to determine the most suitable business structure for your lending venture.